Annuity Mortgage

An annuity mortgage, also known as a repayment mortgage, is a type of home loan in which the borrower pays a fixed monthly amount that includes both interest and repayment of the principal. These combined payments are known as the ‘annuity’. The monthly payments remain consistent throughout the loan term, which usually spans 20 to 30 years and the interest paid can be deducted from tax. An annuity mortgage is a popular choice as it offers a predictable and stable way to pay off the loan over a set period of time.

I would like adviceThe advantages of an annuity mortgage

An annuity mortgage is one of the most common types of home loans in the Netherlands. The other popular option is the linear mortgage. Both annuity and linear mortgages have the advantage of being fully repaid at the end of the loan term, without requiring additional insurance for repayment. Moreover, annuity mortgages offer several benefits, including:

- Consistent monthly payments that facilitate budgeting

- Accumulation of savings through principal repayment

- Low upfront costs due to low initial principal repayment

- Reduced risk of interest rate increases later in the loan term as the outstanding balance decreases

The disadvantages of an annuity mortgage

Annuity mortgages, like any other type of mortgages, have some disadvantages which you should take into consideration.

- Monthly repayments include both mortgage and interest, which may result in higher initial payments

- A relatively high interest rate is paid in the beginning as the debt balance is still large

- The capital repayment increases in size over time while the interest component decreases

- As the interest rate decreases, the mortgage interest deduction also decreases

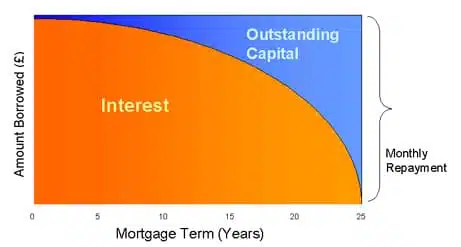

The graph illustrates that while the monthly payments remain constant, the composition of these payments shifts throughout the mortgage term. Initially, the majority of the payments consists of interest, with only a small portion going towards capital repayment. However, as the term progresses, the interest component decreases and a greater portion of the payments goes towards paying off the capital.

Other factors to take into account when choosing your mortgage

An annuity mortgage may not be the best fit if you plan to work part-time or stop working altogether because your monthly payments remain the same. In this case, a linear mortgage may be more suitable because payments decrease over time. Keep in mind that while initial payments may be higher, you will also be paying off more of your capital in the early stages.

When evaluating mortgage options, it is important to consider factors beyond the type and interest rate. These factors may include the ability to make additional payments without penalty, fees associated with taking out the mortgage, penalties for early repayment, and any additional costs such as insurance required by the mortgage provider. A comprehensive evaluation of all these factors can help you make an informed decision when choosing a mortgage.

Want to know more about an annuity mortgage?

Are you interested in learning more about an annuity mortgage and determining whether this is the best option for you? At FVB de Boer, we specialise in providing expert mortgage, pension, and financial advice to expats. We understand the unique challenges and obstacles expats may face when making financial decisions abroad. Contact us today for personalised, independent guidance.

Frequently asked questions about an Annuity mortgage

An annuity mortgage, also known as a repayment mortgage, is the most common type.

The lender works out the amount you need to repay each month to clear your mortgage by the end of an agreed term. Your monthly repayment is made up of two parts:

An interest payment on the loan (will reduce over time)

A capital repayment (increases over time)

In the early years, most of your repayments will go toward paying off interest on your mortgage. But as your mortgage reduces, the interest part of the repayment goes down. So as time goes on, more of your monthly repayments go toward paying off the capital.

You can usually choose either a variable rate or a fixed rate annuity mortgage or in some cases a mixture of both (known as a split rate).

In the early years of the mortgage period, the annuities mortgage usually has lower monthly payments than a linear mortgage.

An annuity mortgage (or repayment mortgage) is a mortgage whereby you pay a fixed monthly amount made up of interest and capital repayment. That interest and repayment together are called the annuity. The monthly amount remains the same throughout the term of the mortgage, which is normally taken out for between 20 and 30 years.

Another popular mortgage type is the lineair mortgage. It is good to know where these types of mortgages differ the most from each other:

- Where as the payments in the linear mortgage are higher in the first couple of years, with the annuity mortgage your monthly repayments stay the same.

- The total cost of an annuity mortgage is higher than the total cost of a linear mortgage, as you pay a higher amount in interest. However, the monthly costs of an annuity mortgage are initially lower. That is why most starters choose an annuity mortgage.

How can we help you?

José de Boer

Financial Advisor

Give us the call and let our team help you plan

the next financial step in your life

Other Services

Mortgage Advisors

At FVB de Boer, we have established good working relationships with a number of Dutch banks to help you realize your dream property.

Home Insurance

FVB de Boer helps you to secure your property with building and fire insurance or home contents insurance for the short or long term.